Separate Business & Personal Finances — Here's Why It's Non-Negotiable

There's a conversation I find myself having over and over again with business owners.

It usually starts with something like, "I know I probably should have done this a long time ago…" And then they tell me that their business income runs through their personal checking account. Their business expenses are scattered across two or three personal credit cards. And come tax time, they — or their bookkeeper — spend hours trying to untangle what was personal and what was business.

If that sounds familiar, I want you to hear this without any judgment: you are not alone. This is one of the most common financial habits I see in small businesses. But it is also one of the most important to correct — and the sooner, the better.

Here's why separating your business and personal finances isn't just good advice. It's non-negotiable.

You Can't Steer What You Can't See

The most immediate benefit of separating your finances is pure, simple clarity.

When everything runs through one account, you have no real picture of how your business is performing. You can't quickly answer: Is my business profitable this month? How much did I actually spend on operations? Am I ahead or behind compared to last year? Those answers are buried under grocery runs, family dinners, and Netflix subscriptions.

A dedicated business account acts as a live ledger of your business's financial health — every deposit a record of revenue, every withdrawal a documented expense. When those lines are clean, leading your business well becomes dramatically simpler.

The IRS Is Paying Attention

This is where the stakes get very real. The IRS requires clear documentation of business income and expenses. When your business transactions are mixed in with your personal ones, two things happen: you miss deductions you're legally entitled to, and you wave a red flag that invites scrutiny.

Approximately 50% of small business owners who mix personal and professional funds face unnecessary tax liabilities as a result. Valid business expenses — a client meal, a software subscription, a mileage reimbursement — become harder to defend when they're buried in a personal account. Separate finances don't just make tax season easier. They protect you if you're ever audited.

Your Personal Assets Are on the Line

If your business is structured as an LLC or corporation, you already have legal protection — a "corporate veil" — that separates your personal assets from your business liabilities. But here's what many business owners don't realize: commingling your finances can pierce that veil.

If you're depositing personal income into your business account, or paying personal expenses with your business card, you may be inadvertently dismantling the legal protection you set up your business structure to provide. In a lawsuit or financial dispute, a court can hold you personally liable if your finances were never truly kept separate. That means your home, your savings, your personal assets — all potentially exposed.

Good stewardship means protecting what you've built. Separation is how you do it.

It Builds Your Business Credit — Separately From Yours

Your business deserves its own financial identity and its own credit history. When you establish a dedicated business account and business credit card, your business begins building a credit profile completely independent of your personal score.

This matters more than most people realize. When the day comes that you need a business loan, want to lease commercial space, or apply for a line of credit to manage cash flow — lenders will look at your business credit history. If that history doesn't exist because everything ran through your personal accounts, you're starting from zero at exactly the wrong moment. Start building now, even if you don't need it yet.

It Signals That You're the Real Deal

There's also a professionalism factor that's easy to overlook. When a client writes a check to your personal name rather than your business name, or when a vendor sees a personal Venmo account instead of a business payment link, it subtly undermines the credibility of the business you've worked so hard to build.

A dedicated business account, operating under your company name, tells every vendor, client, and partner that you take your business seriously. It communicates stability and intentionality — and those signals matter, especially when you're trying to grow.

How to Get This Done — Starting This Week

The good news is that this is one of the easiest financial corrections you can make. Here's where to start:

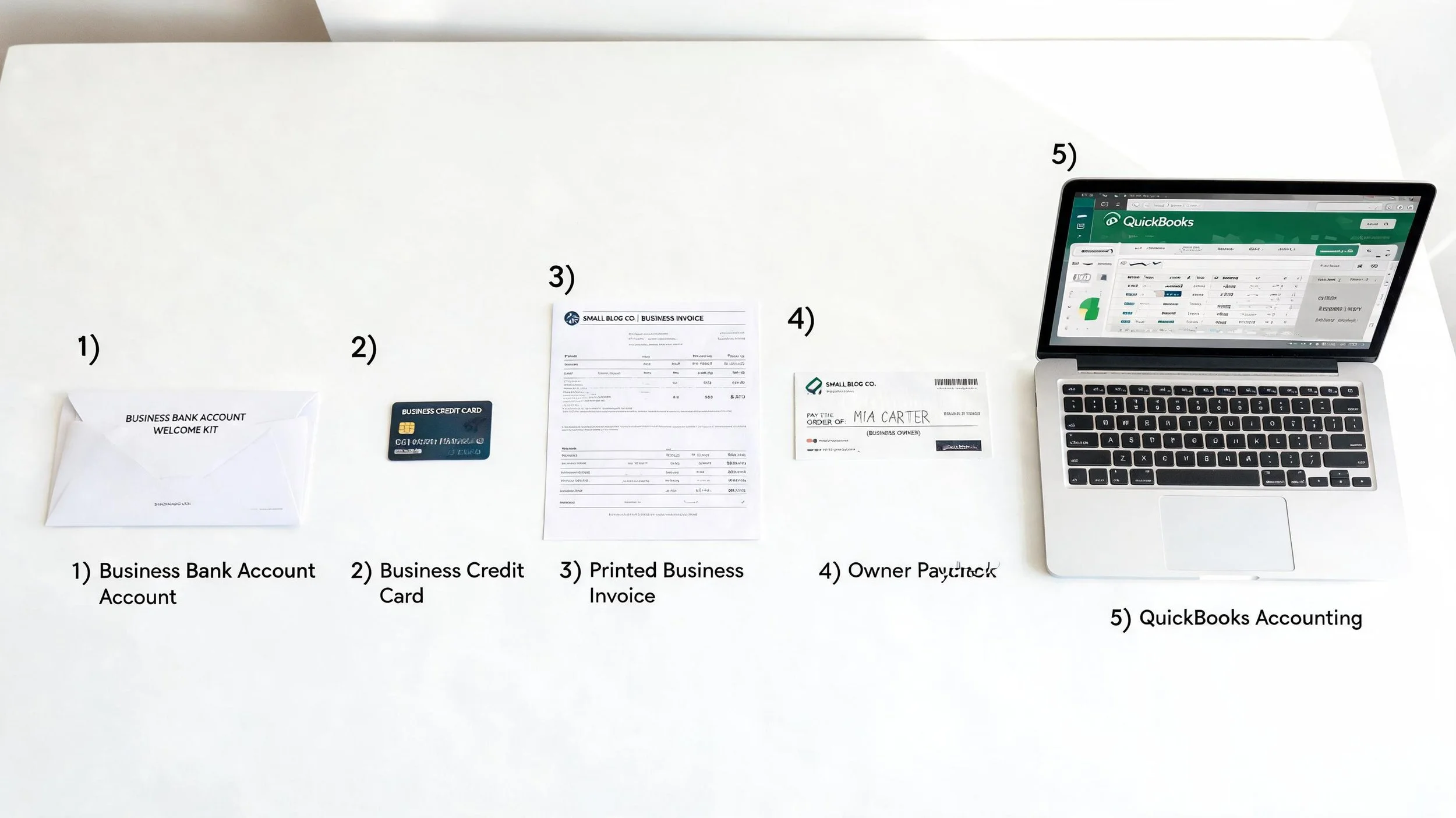

Open a business checking account at your local bank or credit union. Bring your EIN (Employer Identification Number), your business formation documents, and a government-issued ID. Most accounts can be opened in under an hour.

Apply for a business credit card to handle recurring expenses and build your business credit history separately from your personal credit.

Route all business income to the business account from this day forward. Invoices, client payments, online transactions — all of it goes there.

Pay yourself a salary or owner's draw from the business account into your personal account. This simple step clarifies exactly what it costs to run your business — and what you actually take home.

Connect your new account to your bookkeeping software — QuickBooks, Xero, or Wave — so transactions sync and categorize automatically from day one.

A Foundation Worth Building On

Scripture reminds us that a wise builder counts the cost before he builds. Running a business with mixed finances is like building on an unstable foundation — it may hold for a while, but it becomes increasingly fragile over time.

Separating your business and personal finances is not a complicated step. But it is a foundational one. It brings clarity, protection, credibility, and peace of mind. And once it's done correctly, everything else in your bookkeeping becomes easier.

You don't have to figure this out alone. At [Your Company Name], we help business owners get set up right from the very beginning — clean accounts, connected software, and a clear financial foundation that supports everything you're building.