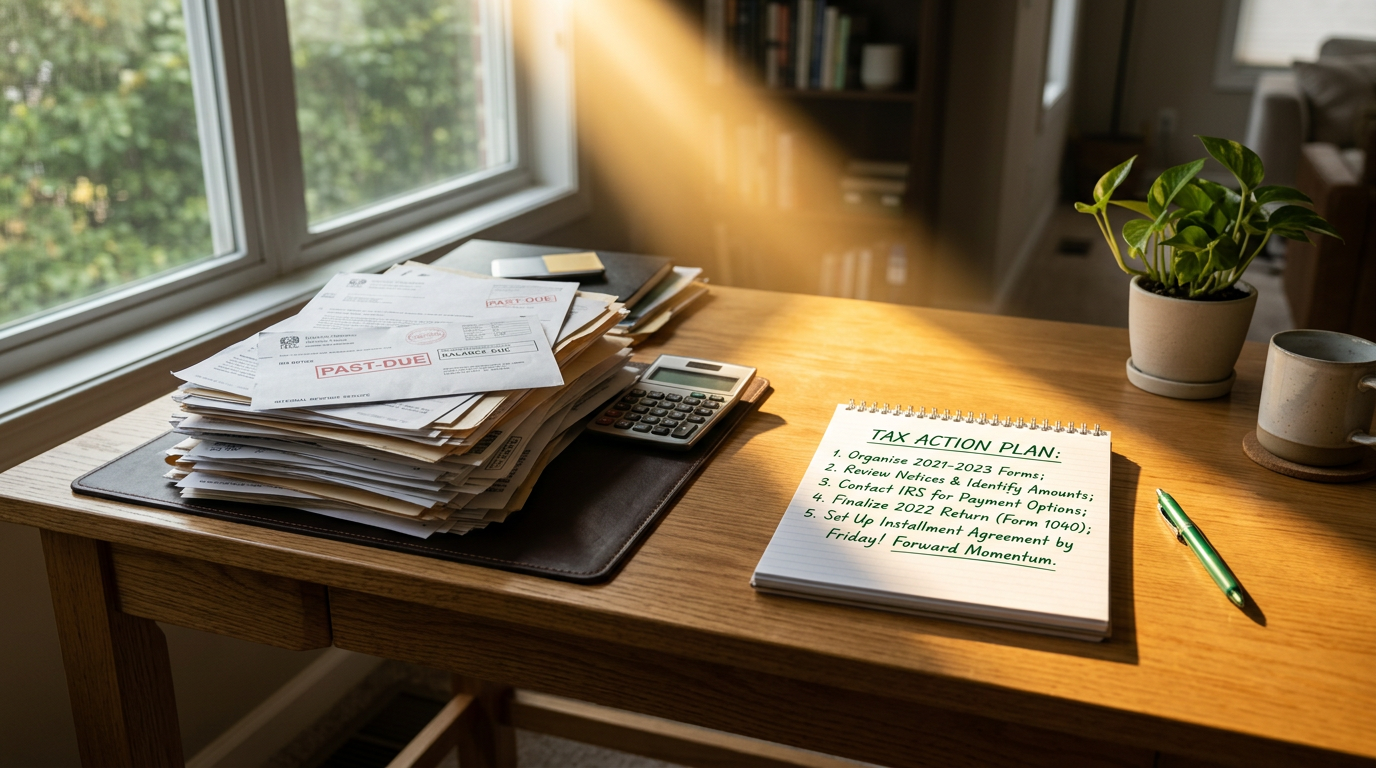

What to Do If You've Fallen Behind on Your Taxes

If you've fallen behind on your taxes, take a breath: this is serious, but it is fixable. The IRS and Taxpayer Advocate Service both emphasize that taxpayers who cannot pay in full still have options, including payment plans, temporary collection delays, and in some cases an offer in compromise.

As a business owner, it's easy to carry shame when the numbers got away from you. But shame clouds judgment, and what you need right now is clarity, honesty, and a step-by-step path forward.

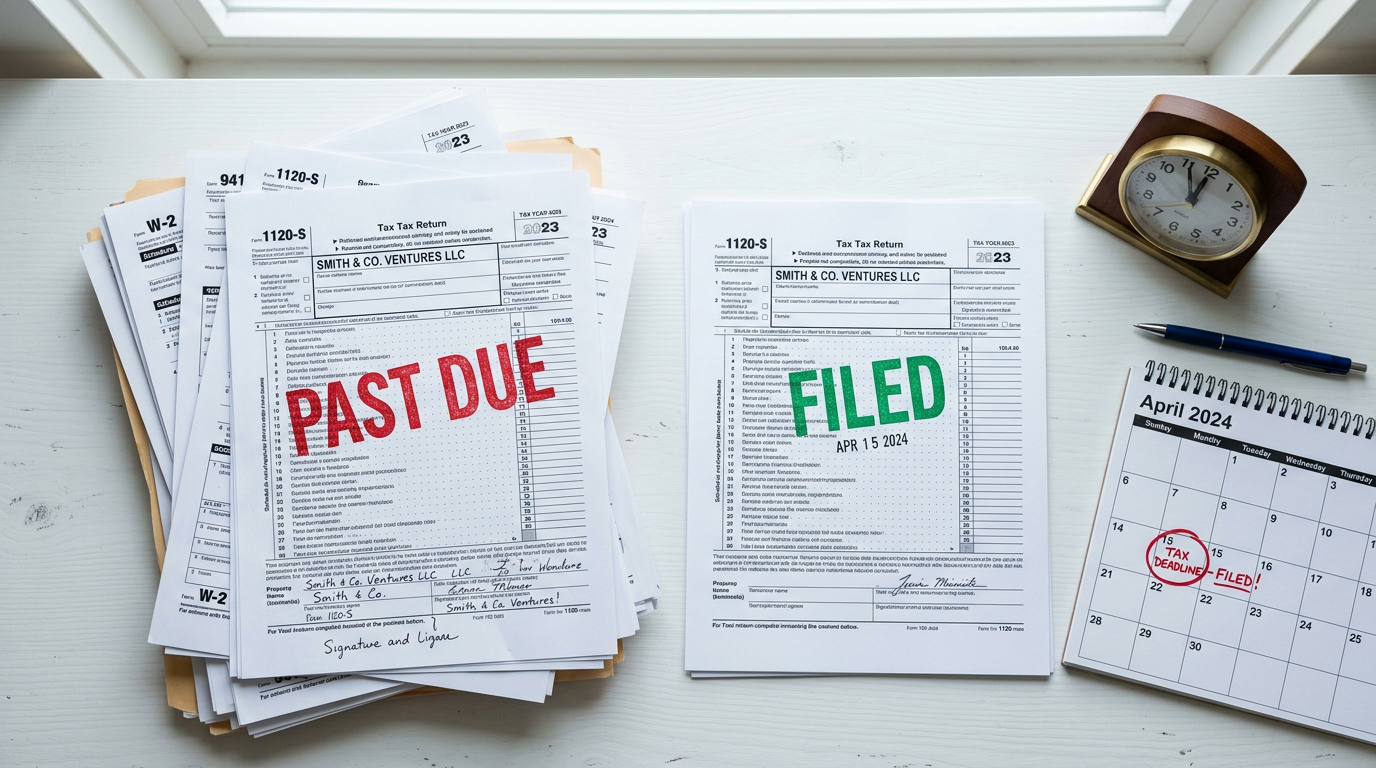

First, file everything

Your first priority is to make sure all required tax returns are filed, even if you cannot pay the full amount yet. Filing on time, or filing as soon as possible if you are late, helps reduce the damage because failure-to-file penalties are generally worse than failure-to-pay penalties.

Do not wait until you have all the money before you file. The IRS specifically says taxpayers who cannot pay in full should still file their return or request an extension by the deadline.

Get current this year

One mistake many business owners make is focusing only on old tax debt while continuing to fall behind in the current year. The IRS generally wants you in current filing and payment compliance before approving longer-term relief options.

That means making current estimated tax payments, payroll tax deposits, or other required filings now. Catching up on the past while staying current in the present is what stops the hole from getting deeper.

Get current this year

One mistake many business owners make is focusing only on old tax debt while continuing to fall behind in the current year. The IRS generally wants you in current filing and payment compliance before approving longer-term relief options.

That means making current estimated tax payments, payroll tax deposits, or other required filings now. Catching up on the past while staying current in the present is what stops the hole from getting deeper.

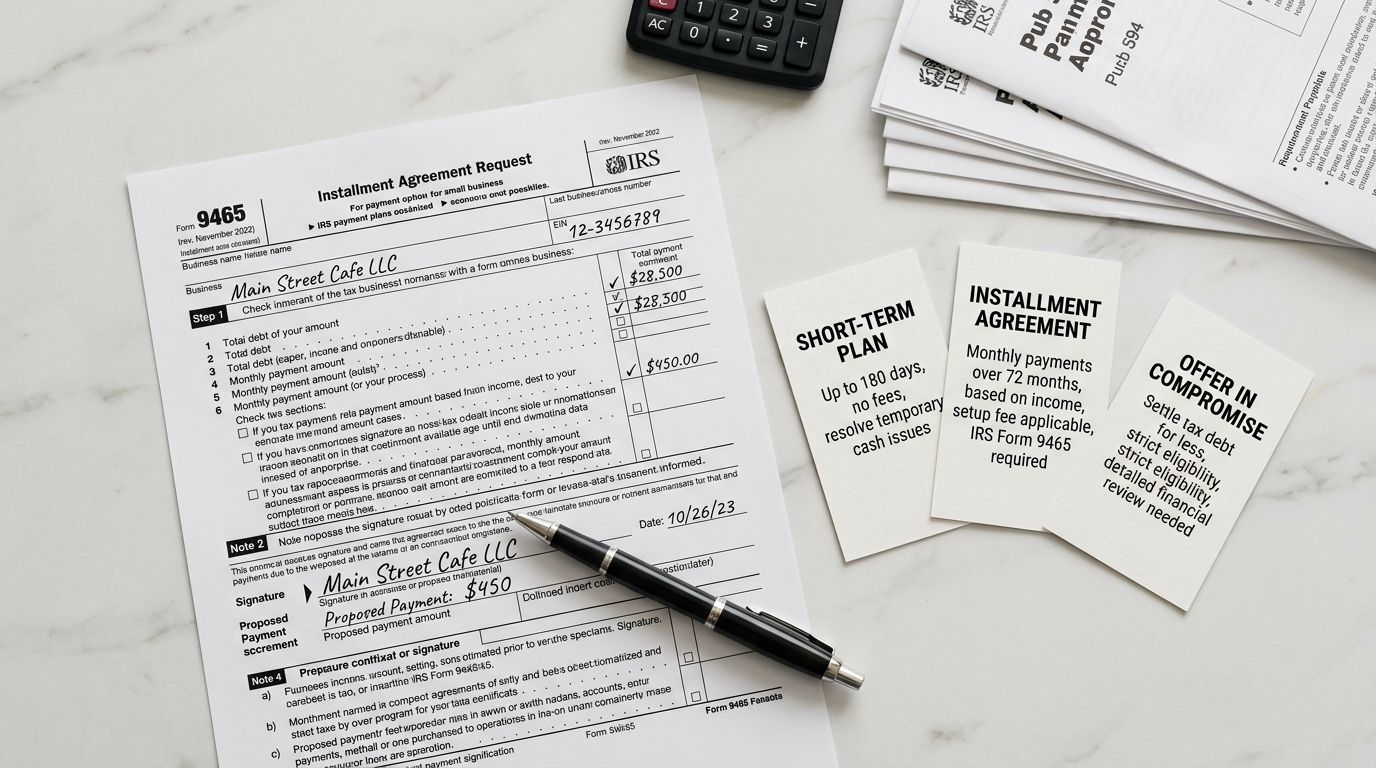

Choose the right IRS option

If you cannot pay in full, the IRS offers several structured options. A short-term payment plan may be available if the total balance owed is less than $100,000 in combined tax, penalties, and interest, giving up to 180 days to pay.

Longer installment agreements are also available in many situations, and the IRS has expanded simple payment plan options for some businesses. For businesses, eligibility can depend on whether the debt involves trust fund taxes and on the total assessed balance.

If paying anything right now would create real financial hardship, the IRS may temporarily delay collection. And if you truly cannot pay the full amount, an offer in compromise may allow settlement for less than the full balance, though the IRS reviews income, expenses, assets, and overall ability to pay very carefully.

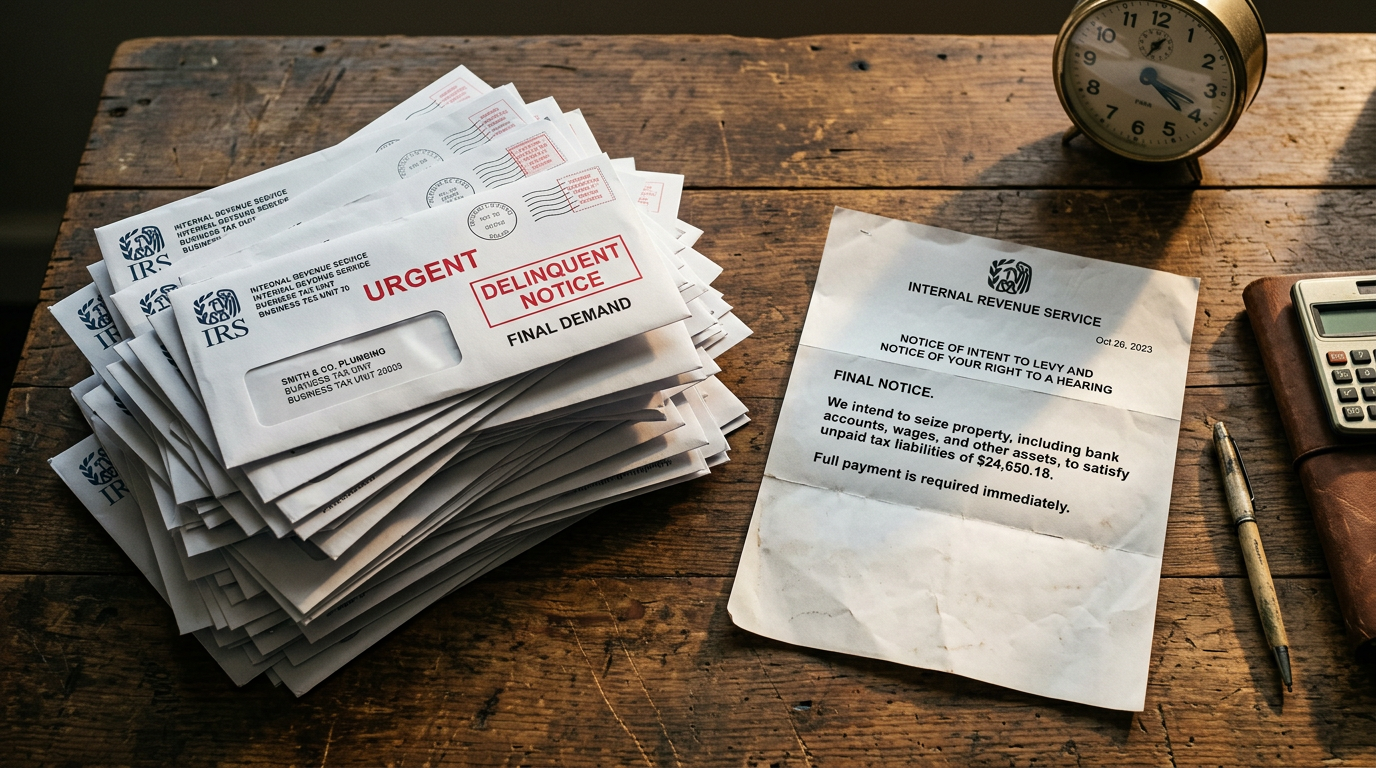

Do not ignore IRS notices

Silence is almost always the most expensive response. If you ignore notices, penalties and interest continue to build, and the IRS may move further into the collection process.

Responding early gives you more options, more time, and more control. The best position is not perfection; it is cooperation.

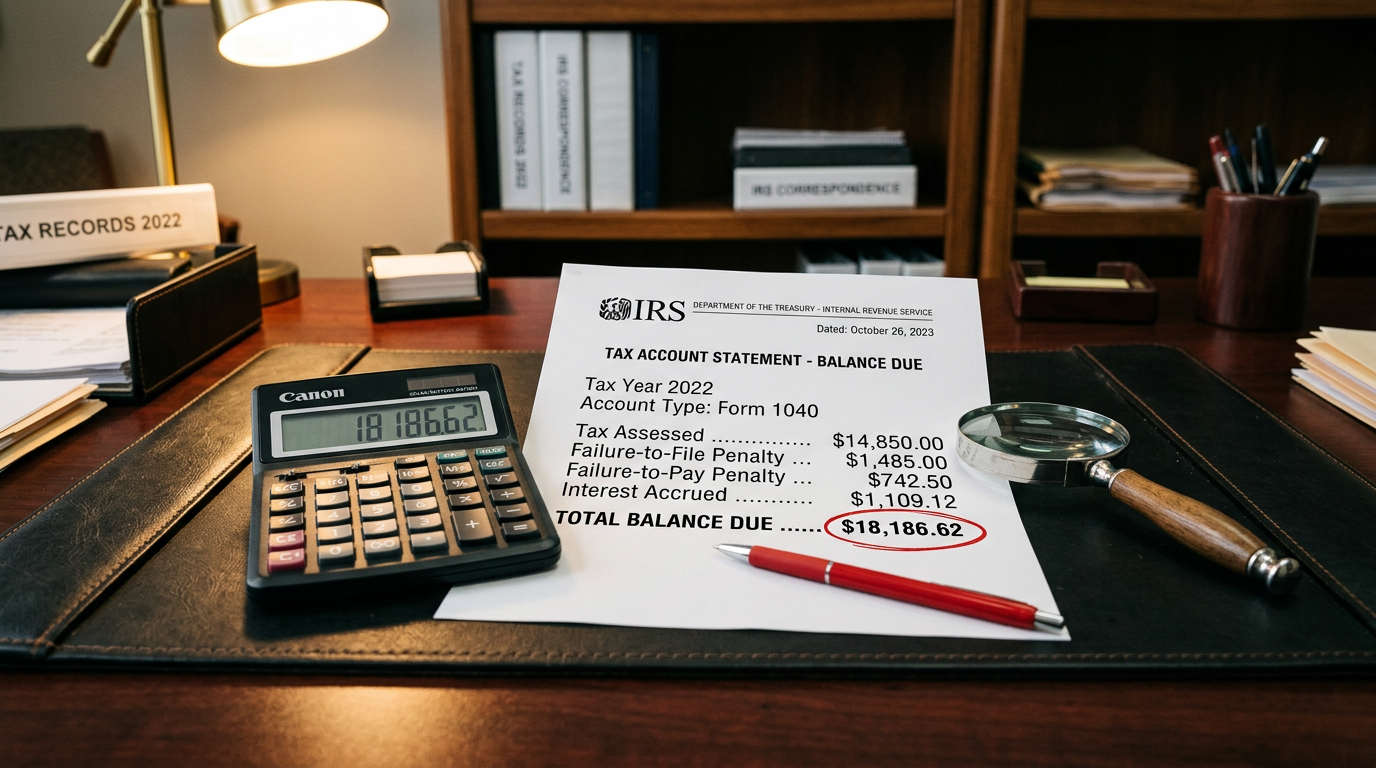

Gather your paperwork

If you want help catching up, good records will save time and money. Gather copies of filed and unfiled returns, IRS notices, bank statements, payroll records if applicable, receipts, loan statements, and a current picture of your business income and expenses.

If you pursue a hardship option or an offer in compromise, you will likely need to provide detailed financial information. The Taxpayer Advocate Service notes that this can include income, expenses, assets, and bank account details, along with forms such as Form 656 in OIC cases.

A shepherd's word here

If you're behind, I want to say this plainly: being behind on taxes does not mean you are a failure. It means something got neglected, delayed, misunderstood, or overwhelmed, and now it needs attention. The answer is not panic; the answer is action.

Wise stewardship begins with truth. We name the problem honestly, we stop the bleeding, and then we walk a steady path toward resolution.

We can help you catch up

You do not have to sort through this alone. A good plan usually starts with four steps: get every return filed, verify the real balance, get current on this year's obligations, and choose the best IRS resolution path for your situation.

If you want a calm, experienced guide to help you untangle the mess, respond to notices, organize the records, and build a catch-up strategy, we can help you catch up.