5 Tax Deductions Most Small Business Owners Miss (And the Money They're Leaving Behind)

Every April, I watch the same thing happen.

Business owners sit down with their tax returns — or hand them off to someone — and they pay their bill without ever asking a critical question: "Did we get everything we were owed?"

Most of the time, the honest answer is no.

Not because anyone did anything wrong. But because no one ever told them what to look for. The tax code is not written for the business owner working 60-hour weeks trying to serve their clients and lead their team. It's dense, it's complex, and the deductions that could save you the most money are often the ones buried deepest.

That's where I come in. Think of this post as your guided walk through five of the most commonly missed tax deductions for small business owners in 2026 — with plain-English explanations and the real dollar impact each one can have. Let's make sure you're not leaving a single dollar on the table that belongs to you.

Deduction #1: The Home Office Deduction

The one most people are afraid to take — but shouldn't be.

If you regularly and exclusively use a dedicated space in your home for business, you are legally entitled to deduct a portion of your home expenses against your business income. That includes a share of your rent or mortgage interest, utilities, homeowner's or renter's insurance, and even repairs made to that space.

Most business owners skip this deduction for one of two reasons: they think it will trigger an audit, or they're not sure they qualify. Neither fear should stop you. The IRS offers a simplified method that lets you deduct $5 per square foot of your dedicated office space, up to 300 square feet — no complex calculations required. If your home office is 200 square feet, that's a clean $1,000 deduction, no receipts needed.

The key word the IRS uses is exclusively. The room must be used for business — not a guest bedroom that also has a desk in the corner. But if you have a true dedicated workspace, this deduction is yours to take. Confidently.

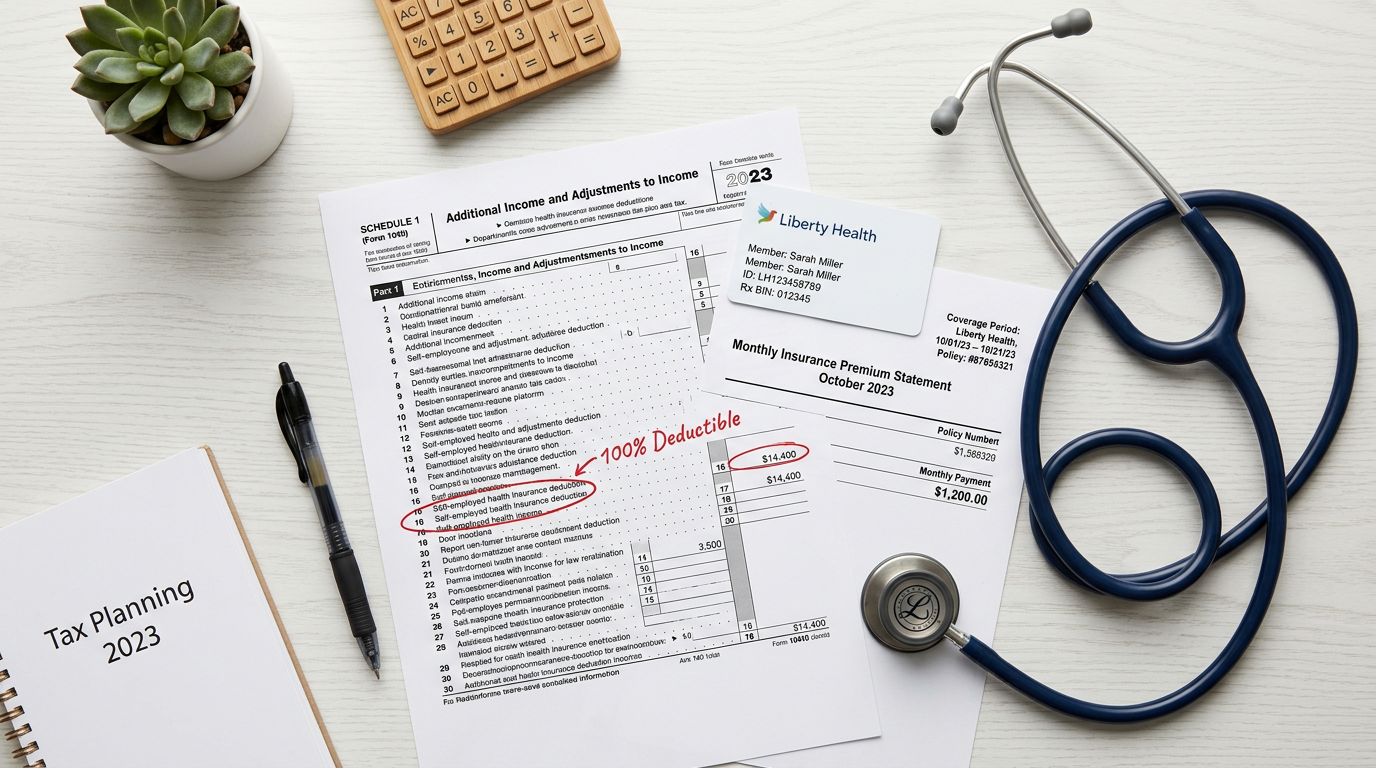

Deduction #2: Self-Employed Health Insurance Premiums

Possibly the most expensive deduction most business owners don't know they have.

If you are self-employed and pay for your own health insurance — for yourself, your spouse, or your dependents — you can deduct 100% of those premiums directly from your income. Not as a business expense on Schedule C. As an above-the-line deduction on your personal return, which means it reduces your adjusted gross income before you even get to itemized deductions.

For a business owner paying $800 a month in health insurance premiums, that's $9,600 per year in deductible expenses that far too many people simply never claim. Dental insurance and long-term care premiums also qualify. If your spouse is covered under an employer plan, different rules apply — but if you're carrying your own coverage, this is one of the most powerful deductions available to you and one of the most frequently missed.

Deduction #3: Retirement Plan Contributions

The deduction that builds your future and reduces your tax bill at the same time.

Here's one of the most beautiful truths in the tax code: the government actually rewards you for saving for your own retirement. Contributions to a SEP-IRA, Solo 401(k), or SIMPLE IRA are tax-deductible — and the limits are generous.

With a Solo 401(k), you can contribute up to $70,000 in 2026 when you combine employee and employer contributions. With a SEP-IRA, you can contribute and deduct up to 25% of your net self-employment income. For a business owner earning $100,000, that could mean a $25,000 deduction — reducing your taxable income dramatically while simultaneously building the retirement security most business owners never stop to plan for.

The tragedy I see is that most business owners are so focused on immediate cash flow that they never set these accounts up. They pay full taxes today and have nothing set aside for tomorrow. You deserve better than that — and the tax code, for once, is on your side.

Deduction #4: Vehicle and Mileage Expenses

The deduction that's hiding in your driveway every single day.

If you use your personal vehicle for business — driving to client meetings, running to the bank, picking up supplies, traveling between job sites — every mile is a deductible expense. In 2026, the IRS standard mileage rate sits at a meaningful per-mile deduction, and it adds up faster than most people realize.

Alternatively, if you purchased a vehicle used for business, the Section 179 deduction allows you to immediately expense the full cost of qualifying vehicles in the year they are placed in service — rather than depreciating them slowly over years. The Section 179 limit for 2026 is $2,560,000, with a phase-out threshold of $4,090,000. Even if you're not buying a fleet of trucks, this provision can apply to a single business vehicle and deliver a substantial one-time deduction.

The catch? You must document your mileage. A simple mileage log — date, destination, purpose, miles driven — is all the IRS requires. There are apps that make this effortless. A year of undocumented mileage is a year of money surrendered unnecessarily.

Deduction #5: Professional Services — Including Your Bookkeeper

The one that literally pays for itself.

This one is personal to me — and I believe it's one of the most overlooked and underappreciated deductions in the tax code.

The fees you pay for accounting, bookkeeping, tax preparation, legal counsel, and business consulting are fully tax-deductible. Every dollar you invest in professional services that support your business operations is a dollar that reduces your taxable income.

Think about what that means practically. If you're in the 22% tax bracket and you pay $3,600 per year for bookkeeping services, your actual after-tax cost is closer to $2,808 — because the IRS is effectively subsidizing the cost of keeping your finances clean. And clean finances, as we've established, are what make all of these other deductions findable in the first place.

It's also worth noting that continuing education, professional development courses, certifications, and workshops directly related to your business are deductible. If you've invested in growing your skills and knowledge as a business owner this year, don't let those receipts go to waste.

The Deductions You Miss Are Not Accidents — They're Gaps

I want to say something directly, because I think it matters.

The IRS doesn't send you a letter saying, "Hey, you missed a deduction." They don't volunteer information that reduces your tax bill. The burden is entirely on you — the business owner — to know what you're entitled to and to document it properly.

That's not a complaint. That's just the reality. And the business owners who respond to that reality with awareness and preparation consistently pay less in taxes — legally, legitimately, and confidently.

The ones who don't? They overpay. Year after year. Often by thousands of dollars.

You work too hard for your money to surrender more of it than you legally owe. My job — as someone who walks alongside business owners as both a financial professional and a pastor — is to make sure that doesn't happen to you.

Let's sit down together, walk through your specific situation, and build a tax strategy that actually works in your favor all year long — not just in April.