How to Build a 90-Day Cash Reserve (And Why It's the Most Important Financial Goal You Can Set)

The businesses that sleep best at night aren't the most profitable — they're the most protected.

The business owners who sleep best at night are not the ones making the most money. They’re the ones with a cash reserve that gives them options when things get hard.

If you’ve ever had a slow month that made your stomach drop, you already understand why this matters.

A 90-day cash reserve isn’t just “nice to have.” It’s the difference between reacting in panic and responding with confidence.

What a 90-Day Cash Reserve Actually Is

Your 90-day number is simple: three months of payroll, rent, and core expenses, saved and ready.

A 90-day cash reserve is exactly what it sounds like: enough liquid cash to cover three months of essential business expenses without relying on new income.

This includes:

Payroll (including your own pay)

Rent or mortgage

Utilities and software subscriptions

Debt payments

Insurance

Core operating costs

To calculate your number:

Add up your average monthly essential expenses.

Multiply that number by three.

If your business needs $15,000 per month to operate, your target reserve is $45,000.

This is your “sleep at night” number.

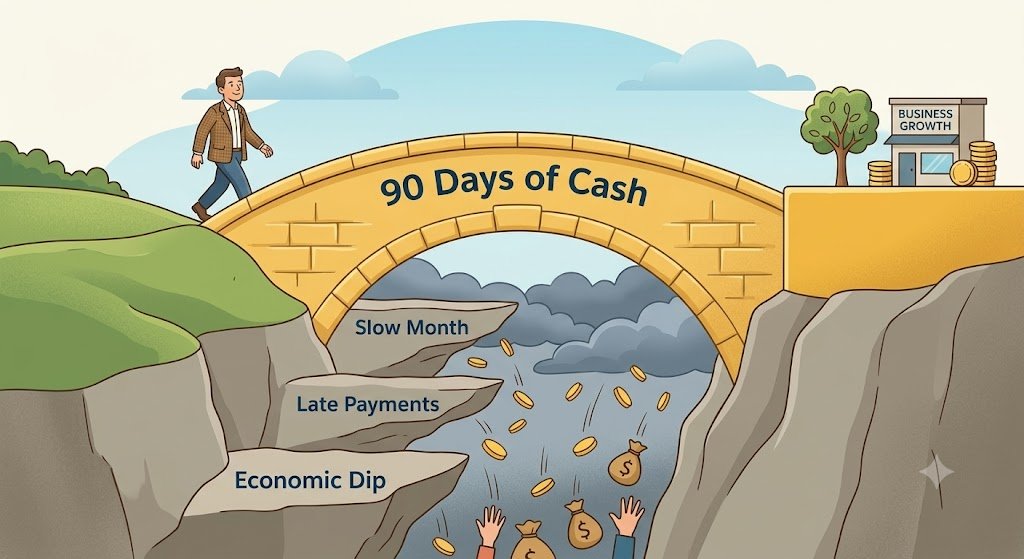

Why 90 Days Is the Standard

A 90-day reserve is the bridge between a rough patch and a real crisis.

Three months isn’t random. It’s long enough to absorb a disruption and short enough to be achievable.

A 90-day reserve protects you from:

Revenue delays (late-paying clients or contracts falling through)

Market fluctuations (seasonal dips or economic slowdowns)

Decision pressure (being forced into bad choices because you’re desperate)

Without a reserve, every problem feels urgent. With one, you gain time—and time gives you better decisions.

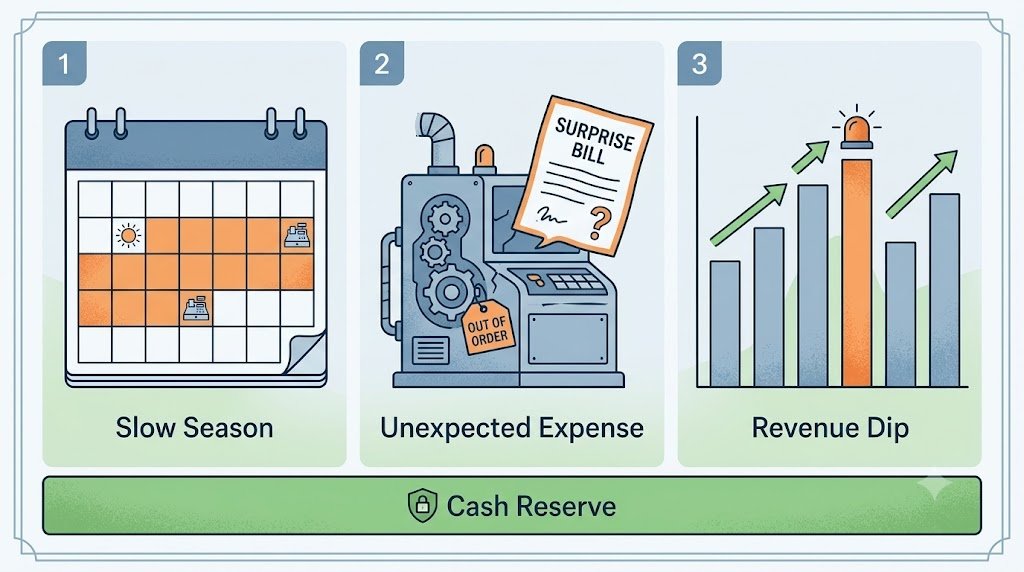

The Three Threats It Neutralizes

Slow season. Surprise bill. Lost client. A reserve turns all three into manageable events.

Every business faces these at some point:

Slow season: Even healthy businesses have predictable dips. A reserve smooths out the valleys so you don’t overreact.

Unexpected expense: Equipment breaks. Taxes surprise you. A reserve absorbs the hit without derailing operations.

Sudden revenue drop: Losing a key client or deal can hurt fast. A reserve buys you time to replace that income strategically.

Without cash reserves, these are crises. With reserves, they’re manageable events.

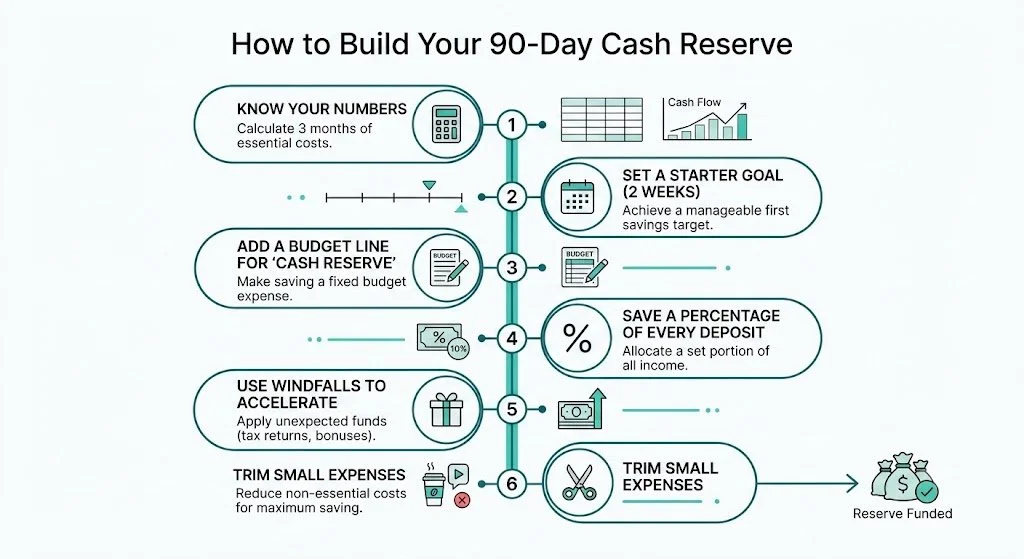

How to Build a Reserve (Even If Cash Is Tight)

You don't need extra cash to start — you need a plan. Here's the six-step path.

If you’re already feeling stretched, building a reserve can sound unrealistic. But it’s more about consistency than large chunks.

Start here:

Get clarity on your numbers

You cannot build what you haven’t defined. Know your true monthly expense baseline.Set a smaller first milestone

Don’t aim for 90 days immediately. Start with 2 weeks, then 30 days, then 60.Create a “reserve line” in your budget

Treat it like a non-negotiable expense—even if it’s small.Skim percentages, not leftovers

Set aside 1–5% of every deposit before spending the rest.Capture windfalls

Tax refunds, strong months, or one-time projects should accelerate your reserve—not inflate your lifestyle.Trim quietly, not dramatically

Look for small, repeatable savings in subscriptions, vendors, or inefficiencies.

Progress compounds faster than you expect.

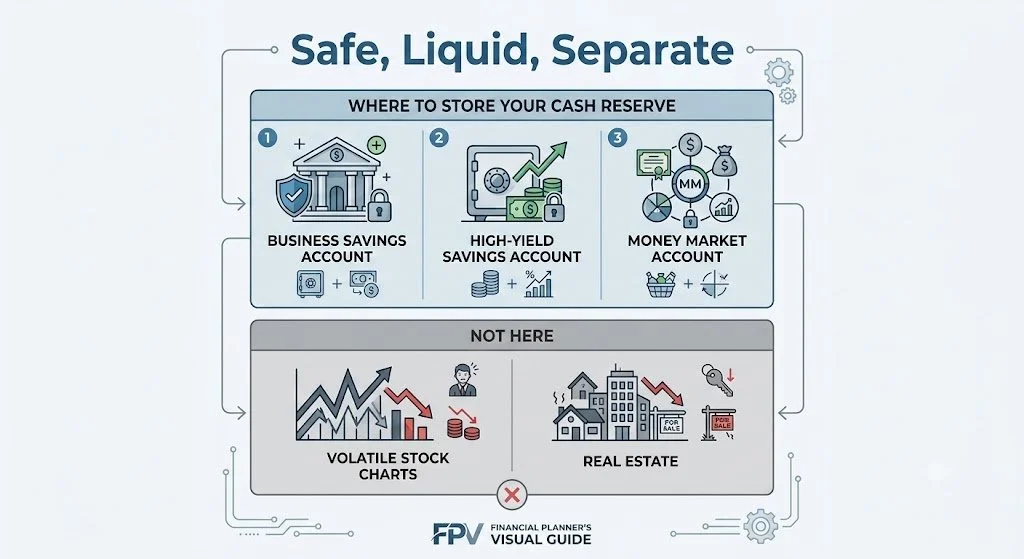

Where to Keep Your Cash Reserve

Liquid. Safe. Separate. That's where your reserve belongs — and nowhere else.

Your reserve should be:

Liquid (easy to access)

Safe (not exposed to market risk)

Separate (not mixed with operating cash)

Best options:

A dedicated business savings account

A high-yield business savings account

Avoid:

Investing it in the market (too volatile for short-term needs)

Keeping it in your checking account (too easy to spend)

Locking it into long-term assets (not accessible when you need it)

This is not growth money. It’s protection.

How Your Bookkeeper Helps You Get This Right

A clear reserve number starts with clean books — that's where your bookkeeper comes in.

Most business owners guess their reserve number—and guess wrong.

A good bookkeeper helps you:

Identify your true monthly expense baseline

Separate essential vs. non-essential spending

Track consistency across months

Build a realistic savings plan based on actual cash flow

Without clean books, your reserve target is just a guess. With accurate data, it becomes a clear, achievable goal.

The Real Value of a Cash Reserve

Same business. Same owner. A completely different level of stress.

A 90-day cash reserve doesn’t just protect your business—it changes how you lead it.

You stop making reactive decisions.

You stop chasing every dollar out of fear.

You start operating from a position of strength.

That’s what financial stability actually looks like.

And it’s within reach.