What Is a Chart of Accounts — And Why Yours Might Be Sabotaging Your Business

Your chart of accounts is the foundation of every financial report your business produces — let's make sure it's built right.

Let me ask you something. When you set up your accounting, did you click through the setup wizard, accept whatever it gave you, and then just start entering transactions? If so, you are not alone — and honestly, I get it. You were focused on running your business, not becoming an accountant. But here is what I need you to hear:

Your chart of accounts is the foundation of every financial report your business produces. If it's wrong — everything built on top of it is wrong too.

That means your Profit & Loss statement? Built on it. Your Balance Sheet? Built on it. The numbers you hand your CPA at tax time? All of it traces right back to that one list you probably never touched.

Let's fix that.

So What Is a Chart of Accounts?

Think of your chart of accounts like a filing cabinet — every transaction needs a home.

In plain English, a chart of accounts is simply a filing cabinet.

Every time money moves in or out of your business, it has to go somewhere — into a folder, a category, a drawer. Your chart of accounts is the master list of all those folders. It tells QuickBooks: "When I pay my electric bill, put it here. When a client pays me, put it there."

Think of it like the table of contents for your entire financial story. If the table of contents is a mess, the whole book is hard to understand.

If your QuickBooks setup looks like this, your reports might not be telling you the truth.

The Problem With QuickBooks Defaults

Here is where most small business owners go sideways. QuickBooks is not dumb — but it's also not psychic.

When you set up your account, QuickBooks generated a default chart of accounts based on your industry type. And while that's a decent starting point, one size absolutely does not fit all. A landscaping company and a consulting firm both might select "Service Business" during setup — but their financial needs look nothing alike.

The result? You end up with accounts you don't need, accounts that are missing, and categories so vague that your reports don't actually tell you anything useful. I've seen business owners who had a single account called "Other Expenses" with tens of thousands of dollars sitting in it. That's not bookkeeping — that's a mystery novel.

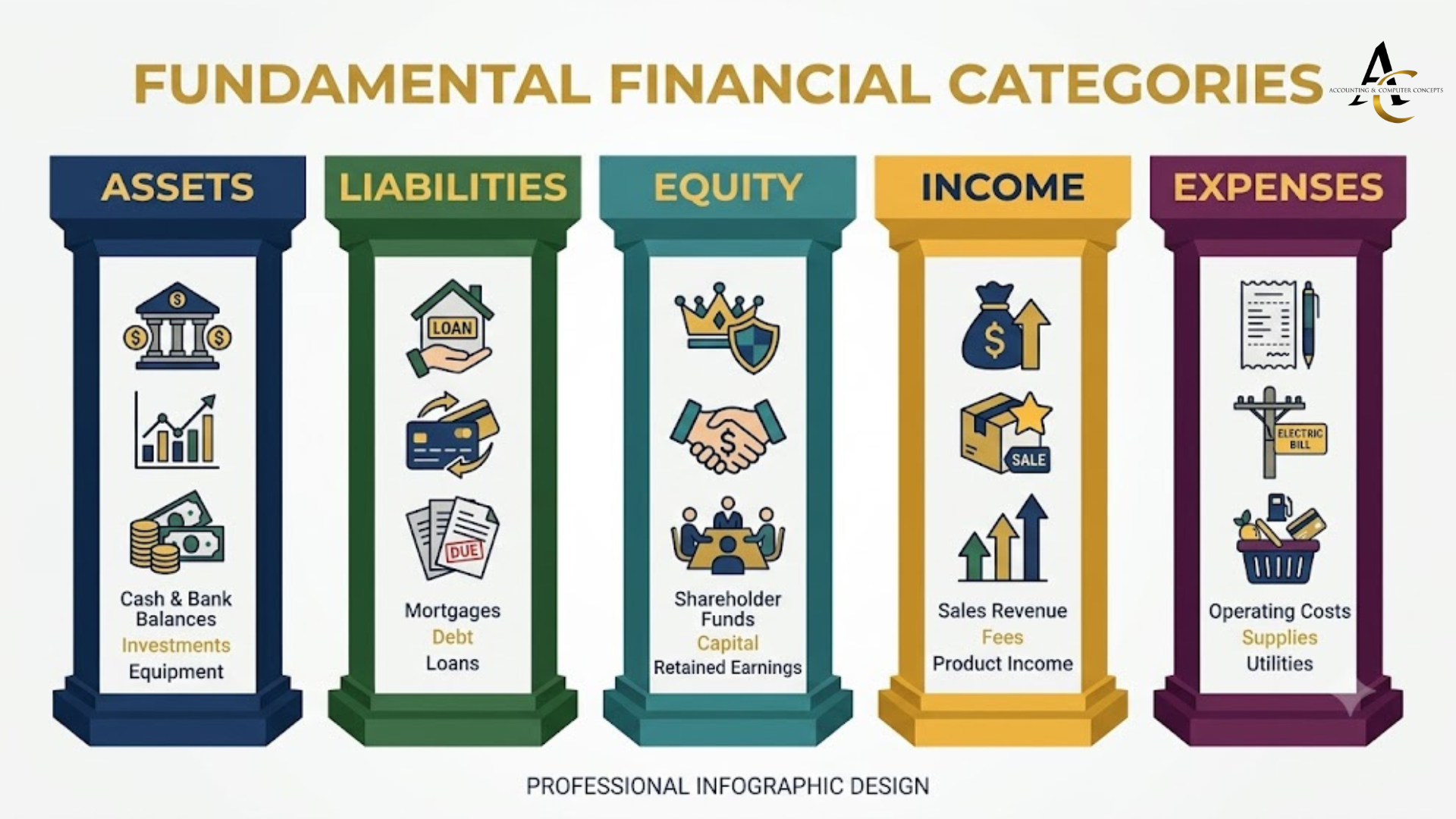

The Five Categories Every Chart of Accounts Must Have

Every chart of accounts — no matter the business — must be built around these five categories.

No matter what kind of business you run, your chart of accounts must be built around five core categories. Here is what each one means and what belongs in it:linkedin+1

Assets — Everything your business owns: checking accounts, savings accounts, equipment, accounts receivable (money customers owe you), and inventory

Liabilities — Everything your business owes: business loans, credit card balances, payroll taxes due, and accounts payable (bills you haven't paid yet)

Equity — The owner's stake in the business: your capital contributions, retained earnings, and owner's draw

Income (Revenue) — Every way money comes into your business: service revenue, product sales, consultation fees — broken out in a way that reflects your actual revenue streams

Expenses — Every way money goes out: rent, payroll, software subscriptions, advertising, professional fees, insurance — the more specific, the more useful

The goal isn't to have a hundred accounts. The goal is to have the right accounts — enough detail to make decisions, not so much that it becomes noise.

A Bad Chart of Accounts Produces Misleading Reports

Here is the part that keeps me up at night when I look at clients' books.

When transactions get dumped into the wrong accounts — or into catch-all categories that don't mean anything — your financial reports stop telling the truth. Your Profit & Loss might show you're profitable when you're actually bleeding money in a specific area. Your Balance Sheet might look healthy while a liability is quietly growing unchecked.

You cannot make good business decisions with bad data. It's like trying to drive across the country with a map of the wrong state. You feel like you're moving, but you're not getting where you need to go.

Real Examples That Cost Business Owners at Tax Time

A disorganized chart of accounts doesn't just create confusion — it can cost you real money when tax season arrives.

These are the kinds of errors I see that turn a routine tax season into an expensive headache:

Meals vs. Travel vs. Entertainment all lumped into one "Other Expense" account — which means your CPA can't apply the correct deduction rules to each category (meals are typically 50% deductible; others may be fully deductible or not at all)

Owner's draws coded as expenses — This is one of the most common mistakes I see. An owner's draw is not a business expense, but if it's sitting in your expense accounts, your profit looks artificially low and your tax picture gets distorted

Loan proceeds coded as income — If you received a business loan and someone categorized it as revenue, congratulations — you may have just told the IRS you made more money than you did

Equipment purchases coded as expenses — Larger asset purchases may need to be depreciated over time, not expensed all at once. How it's categorized determines how it's treated on your return.

Mixing personal and business expenses under the same account — When the lines blur in your chart of accounts, they blur everywhere else too

How to Know If Yours Needs Restructuring

Ask yourself these questions honestly:

When you pull a Profit & Loss report, does it actually show you where your money is coming from and where it's going — in a way that helps you make decisions?

Do you have accounts with names like "Other," "Miscellaneous," or "Ask My Accountant"?

Have you ever accepted QuickBooks' suggested category during bank feed import without questioning it?

Does your CPA have to ask you a lot of questions at tax time because your reports aren't clear?

If you answered yes to any of those, your chart of accounts likely needs attention. The good news is that restructuring it is absolutely doable — and the difference it makes in the clarity and accuracy of your reports is immediate.

You Don't Have to Figure This Out Alone

You don't have to figure this out alone — let's get your books built on a solid foundation.

Your chart of accounts should be built around your business — your revenue streams, your expense categories, your industry, and your goals. It's not a one-time setup item you can ignore. It's the backbone of everything.

If you are not confident that yours is set up correctly — or if you've never really looked at it — now is the time.

👉 Let us set yours up correctly.

We'll review your current chart of accounts, identify what's working and what isn't, and build you a structure that actually reflects your business. So the next time you open a financial report, you can trust what it's telling you.