How to Stay Tax-Ready All Year (Not Just in April)

Let me tell you about the two kinds of business owners I work with.

The first kind calls me in January — or sometimes February, March, or a panicked April 14th. Their receipts are scattered. Their books haven't been touched since last year. And they spend the next several weeks in a fog of stress, scrambling to piece together a year's worth of financial history in a matter of days.

The second kind? They call me throughout the year. We talk in March, in June, in September. Their books are clean. Their deductions are documented. And when tax season arrives, they barely break a sweat.

Here's the secret: the second group isn't smarter or more disciplined than the first. They just learned one thing the hard way — or the easy way, if someone showed them early enough.

Tax readiness is not a season. It's a rhythm.

Let me show you how to build that rhythm into your business — starting today.

The Real Cost of Not Being Prepared

Before we talk about habits, let's be honest about what tax unpreparedness actually costs you — because it's more than just stress.

When your books aren't current, you miss deductions you're entitled to. You can't accurately calculate quarterly estimated payments, which means you either overpay throughout the year — giving the IRS an interest-free loan — or you underpay and face penalties when April comes. You also lose the ability to make strategic financial decisions, because you don't have a clear picture of where your business actually stands.

Being tax-ready all year isn't about paperwork. It's about having the clarity and control to lead your business wisely — all twelve months of the year.

Habit #1: Make Friends With Your Quarterly Deadlines

The foundation of year-round tax readiness is understanding — and respecting — the IRS quarterly estimated tax schedule.

If you are self-employed or a small business owner, the IRS expects you to pay taxes as you earn, not just once a year in April. The 2026 quarterly estimated tax deadlines are:

Quarter Income Period Due Date

Q1 January – March April 15, 2026

Q2 April – May June 16, 2026

Q3 June – August September 15, 2026

Q4 September – December January 15, 2027

Missing these deadlines doesn't just mean a late payment — it means penalties and interest that compound quietly every quarter. The IRS calculates underpayment penalties based on how much you should have paid and when, so the earlier you underpay, the more it costs you.

The simplest way to calculate your quarterly payments is to take your prior year's total tax bill and divide it by four. This "safe harbor" method protects you from underpayment penalties even if your income increases in the current year. For business owners with adjusted gross income over $150,000, the safe harbor threshold is 110% of last year's tax — something many business owners don't realize until they owe a penalty.

Habit #2: Reconcile Your Books Every Single Month

If quarterly deadlines are the skeleton of tax readiness, monthly reconciliation is the heartbeat.

Reconciling your accounts means comparing your internal financial records to your actual bank and credit card statements — every month, without fail. It catches data entry errors, duplicate transactions, missing expenses, and unauthorized charges before they quietly compound into major problems.

The business owners who struggle most at tax time are almost always the ones who let reconciliation slide for months at a time. When you finally sit down to sort through three or four months of unreconciled transactions, you're not just doing accounting — you're doing archaeology. Details fade, receipts disappear, and the process that should take thirty minutes turns into a full day of frustration.

Set a recurring date every month — ideally within the first five business days after the month closes — and treat it like a non-negotiable appointment. Cloud-based tools like QuickBooks Online or Xero make this dramatically easier by syncing bank transactions automatically, so your monthly review becomes a matter of confirming and categorizing rather than manually entering every transaction.

Habit #3: Track Every Deductible Expense As It Happens

The deductions you miss are rarely large ones. They're the $22 parking fee on the way to a client meeting. The $14.99 monthly subscription for business software. The client lunch that never made it into a folder.

Individually, they feel small. Collectively, they represent hundreds — sometimes thousands — of dollars in deductions that disappear simply because no one documented them at the time.

The most effective habit is to capture expenses the moment they happen. Take a photo of every receipt with a mobile app like Dext or the built-in receipt scanner in QuickBooks. Log every business mile with an app like MileIQ or Everlance. If it's a business expense, document it before the day is over. Memory is not a reliable bookkeeping system.

This habit also serves you beyond tax season. When you track expenses consistently, you can see exactly where your money is going month by month — which means you can catch cost leaks early, evaluate spending categories honestly, and make smarter decisions about where to invest and where to cut back.

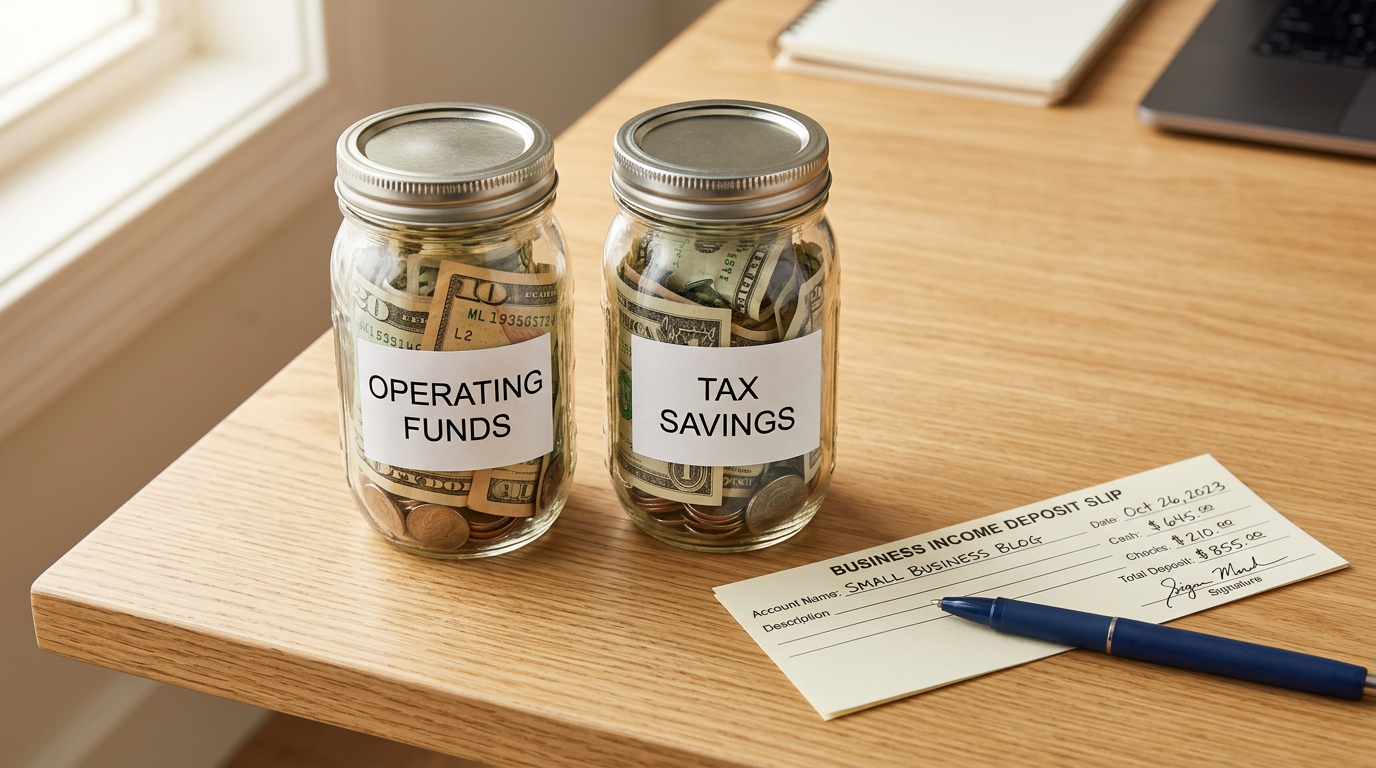

Habit #4: Set Aside Taxes From Every Deposit

One of the most painful conversations I have with business owners involves cash flow — specifically, the moment they realize that the $40,000 sitting in their business account isn't all theirs. A significant portion of it belongs to the IRS, and it's been sitting there all year, silently earmarked for a bill that's coming whether they're ready or not.

The simplest fix is also the most powerful one: every time revenue comes in, move a percentage to a separate savings account designated exclusively for taxes. A common guideline for small business owners is to set aside 25–30% of net profit, though your specific rate will depend on your tax bracket, business structure, and deductions.

This is not a complicated system. It is simply the discipline of treating your tax obligation as an expense — just like rent, payroll, or software — rather than treating everything in your account as spendable income. Business owners who do this consistently never have a panic-inducing tax bill. They have a payment they've been preparing for all along.

Habit #5: Do a Financial Review Every Quarter

Once a quarter — ideally right before each estimated tax payment is due — sit down for a 30-minute financial review. This is the practice that separates business owners who are perpetually reactive from those who are consistently strategic.

Your quarterly review should cover four things:

Revenue trend — Is your top-line income growing, flat, or declining compared to the same quarter last year?

Expense review — Are any cost categories running higher than expected? Are there subscriptions or recurring charges you've forgotten about?

Estimated tax calculation — Based on your current year's net income, are your quarterly payments on track? Do they need to be adjusted up or down?

Deduction audit — Are there any expenses from the past quarter that weren't properly documented or categorized?

This quarterly rhythm keeps you from being surprised by your tax bill, ensures your books are always reasonably current, and gives you the financial clarity to make good decisions about your business throughout the year — not just in hindsight.

Habit #6: Talk to Your Bookkeeper Before December — Not After

Here is one of the most high-value, lowest-effort habits on this list, and one of the most consistently skipped.

A brief conversation with your bookkeeper or accountant in October or November — before the year closes — gives you the opportunity to make strategic financial moves while you still can. That might mean accelerating certain deductible expenses into the current year, making a retirement plan contribution before the deadline, reviewing whether your business structure is still optimal, or timing a major equipment purchase to maximize your Section 179 deduction.

After December 31, those options are gone. The decisions are made by default rather than by design. A thirty-minute planning conversation in the fall can be worth thousands of dollars in tax savings — and it costs you almost nothing except the willingness to be proactive.

Your Year-Round Tax Readiness Rhythm

Here is the simple, repeatable rhythm that will keep you tax-ready every month of the year:

Monthly (30 minutes):

Reconcile all bank and credit card accounts

Review and categorize all transactions

Confirm all receipts are documented

Quarterly (1 hour):

Review revenue and expense trends

Calculate and pay estimated taxes by the deadline

Audit deductions for the quarter

Adjust financial projections for the remainder of the year

Annually (in October/November):

Meet with your bookkeeper for year-end tax planning

Review business structure and elections

Maximize retirement contributions and year-end deductions

Prepare for the upcoming tax year

You Don't Have to Figure This Out Alone

The rhythm described in this post is not complicated. But for a business owner already working sixty-hour weeks, "not complicated" and "easy to actually do" are two very different things.

That's why so many business owners who intend to stay on top of their finances still find themselves in the same scramble every April. Not because they're disorganized people. Because bookkeeping is not why they got into business — and every hour spent on their books is an hour not spent serving clients, growing their team, or building what they started this company to build.

If you want a bookkeeping partner who keeps your books clean, your quarterly taxes accurate, and your financial reports ready every month — that's exactly what we do.

Download our free Tax Prep Checklist below — it's the same checklist we walk our own clients through every quarter, and it will show you exactly where you stand and what needs attention before the next deadline.

And if you want to hand this off entirely and never scramble at tax time again, we'd love to talk.