What Is Working Capital — And Why Every Business Owner Needs to Understand It

This is what working capital looks like on a real balance sheet — the green highlights are your current assets, the red are your current liabilities. The gap between those two numbers is the number that matters most.

There's one number in your business that determines whether you can survive a slow month, an unexpected bill, or a growth opportunity. Most business owners have never calculated it.

A few months ago, I sat down with a small business owner who was frustrated and confused. Her business was profitable — she could see that. Her accountant had told her so. But she was stressed about money constantly. She couldn't figure out why every unexpected expense felt like a crisis. Sound familiar?

When we pulled up her balance sheet and calculated her working capital, the answer was right there. She had profit on paper but almost no liquidity in real life. One number told the whole story — and once she understood it, everything changed.

That number is working capital. And today, I'm going to show you exactly what it means, how to find yours, and what to do if you don't like what you see.

What Is Working Capital, Really?

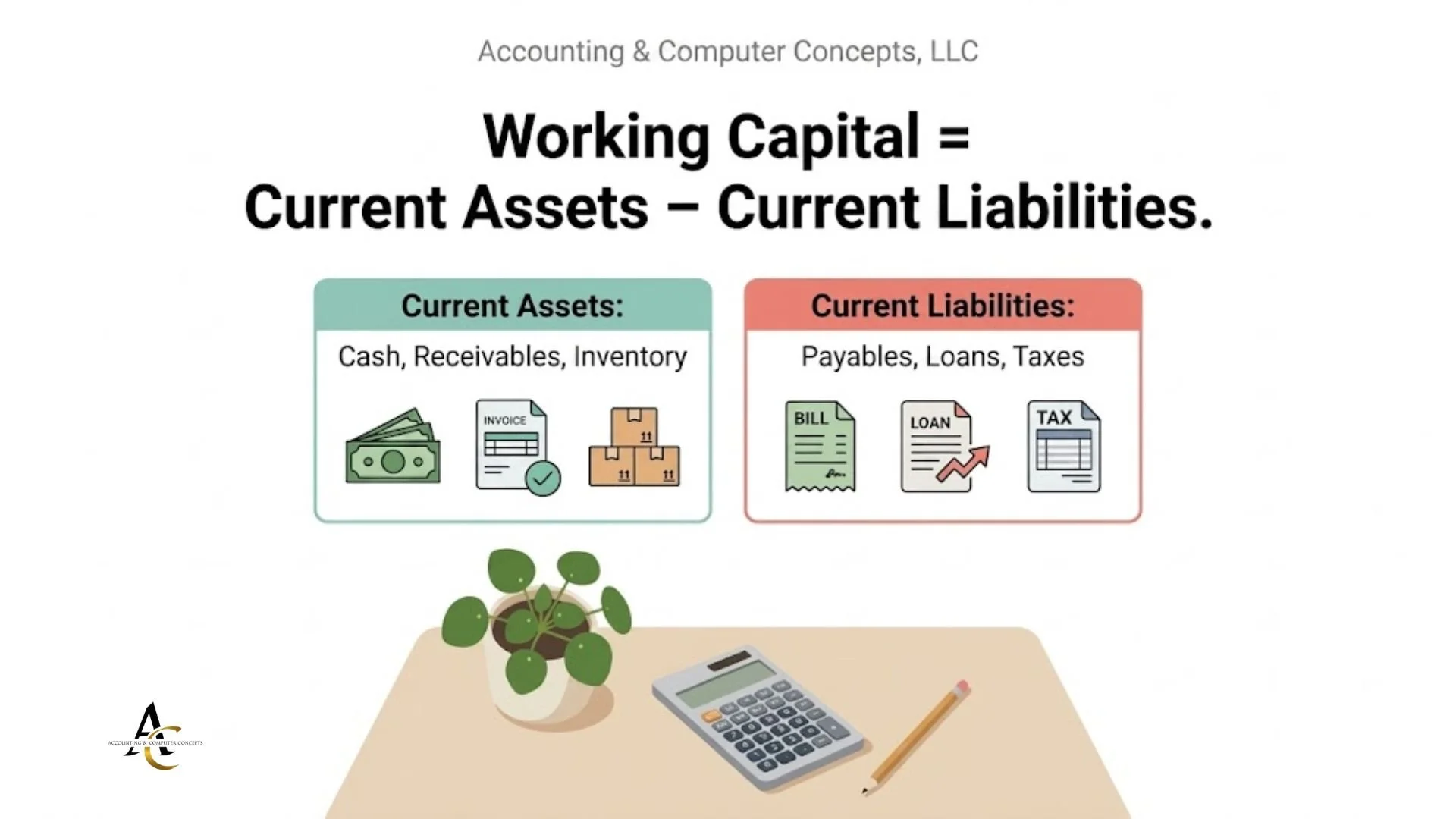

The formula is simple. The implications are enormous. Working Capital = Current Assets − Current Liabilities. That single calculation tells you whether your business can survive what's coming next.

Working capital is the money available to keep your business running day to day. The formula is dead simple:

Working Capital = Current Assets − Current Liabilities

Current assets are things you can turn into cash within the next 12 months — your bank balance, money clients owe you, and inventory on hand.

Current liabilities are what you owe within the next 12 months — vendor bills, short-term loans, payroll, upcoming taxes.

Subtract one from the other. That's your number. Simple math, massive implications.

Why Working Capital Beats Profit Margin in a Crisis

Here's the hard truth most people don't hear until it's too late: you can be profitable and still run out of cash.

Picture this — you land a great project in January and invoice $40,000. But your client pays in 90 days. Meanwhile, payroll is due Friday, rent is due the 1st, and your supplier wants payment now. Your profit looks great on paper. Your bank account is screaming.

Working capital measures your right-now ability to meet right-now obligations. Profit tells you how the story ended. Working capital tells you whether you can survive the next chapter. In a cash crunch, working capital is the only number that matters.

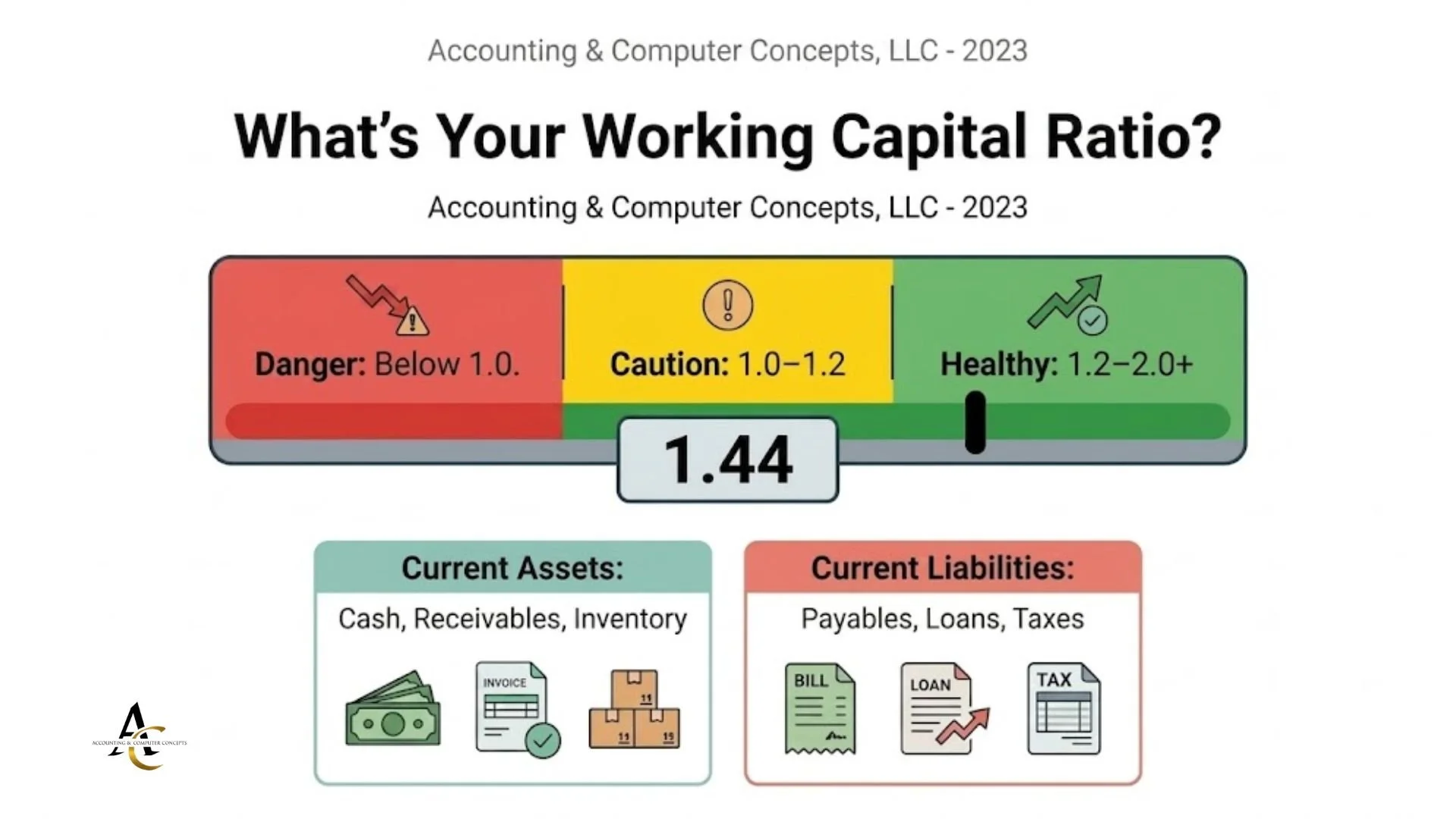

Where does your number fall on this scale? A ratio between 1.2 and 2.0 means your business has the cushion it needs. Below 1.0 is a warning sign that deserves immediate attention.

What Does "Healthy" Actually Look Like?

Meet the working capital ratio:

Working Capital Ratio = Current Assets / Current Liabilities

Here's how to read it:

Below 1.0 — Danger zone. You owe more than you have, and one surprise expense can tip you over

1.0 to 1.2 — You're surviving, but there's almost no cushion for anything unexpected

1.2 to 2.0 — This is the sweet spot. Healthy, resilient, and room to breathe

Above 2.0 — Strong position, but worth asking if that cash could be working harder

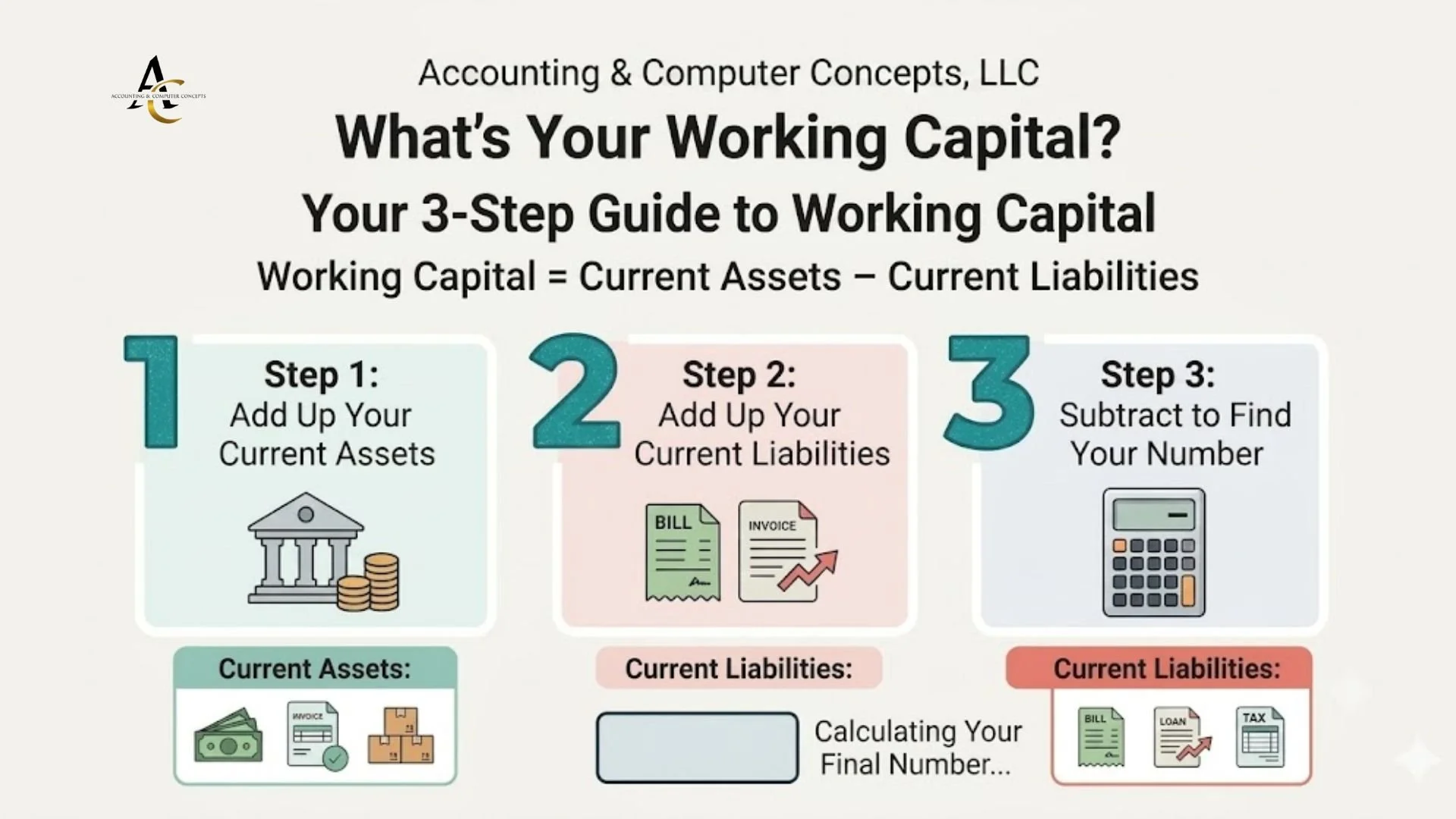

Calculate Your Working Capital in Under 5 Minutes

You don't need a finance degree for this. Three steps. Under five minutes. And you'll know more about your business's financial health than most owners ever bother to find out.

Open your bookkeeping software or pull your most recent balance sheet. Here's all you need to do:

Add up your current assets — cash on hand, receivables, inventory, prepaid expenses

Add up your current liabilities — credit cards, short-term loans, payroll owed, upcoming tax bills

Subtract liabilities from assets

That's your working capital. Then divide assets by liabilities for your ratio. You've now done something most business owners never do — and you're already ahead.

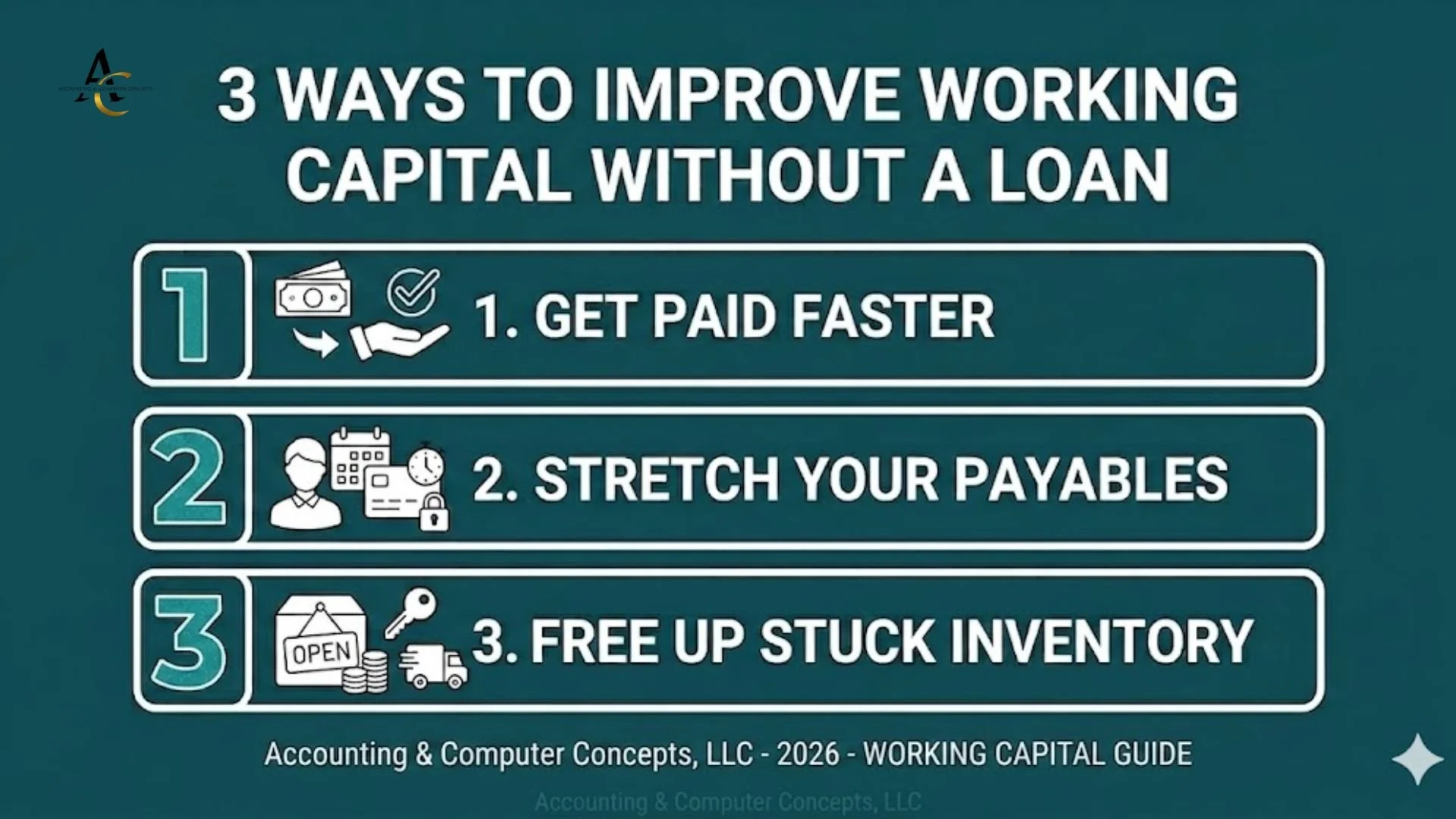

Three Ways to Improve Working Capital Without Taking Out a Loan

You don't always need more money. Sometimes you just need to move the money you already have more strategically. These three moves can shift your working capital position without borrowing a single dollar.

Good news: you often don't need more money. You need to move the money you have more intentionally.

Get paid faster — Invoice the moment a job is done, shorten payment terms, and follow up on anything overdue. Cash sitting in a client's account isn't helping your business

Stretch your payables (strategically) — Ask vendors for longer payment windows. Paying in 45 days instead of 15 keeps cash available longer without burning relationships

Free up stuck inventory — Inventory on a shelf is cash on a shelf. A quick promotion or bundle deal can turn stagnant stock into working capital fast

What Negative Working Capital Really Means

If your number is negative, take a breath — but take it seriously.

Negative working capital means your short-term debts outweigh your short-term assets. For some large retail businesses with reliable supplier terms, this is manageable. For most small businesses, it's a warning light that needs attention now, not later.

The earlier you catch it, the more options you have. Waiting turns a fixable problem into a full-blown emergency. The business owners who recover quickly are the ones who got honest about their numbers before the crisis hit.

You Can't Manage What You Haven't Measured

I know you're busy running your business. The books often end up being the last thing you look at — and the financial metrics that protect everything you've built get pushed to the background.

You don't have to figure this out alone. We pull up the books together, calculate your number, and give you a clear picture of where you stand — and what to do next.

But working capital is one number. One calculation. And it tells you more about the real health of your business than almost anything else on your balance sheet.

Now you know how to find it. The only question is — what does yours say?

If you're not sure, that's exactly what we're here for. Let's sit down together, pull up your books, and review your working capital so you know exactly where you stand — and have a clear plan for what comes next.