Why Your Business Is Profitable But Still Cash-Poor

It is one of the most confusing, frustrating, and honestly demoralizing experiences a business owner can have.

You look at your Profit & Loss statement and the numbers look good. Revenue is up. You landed new clients. By every visible measure, you're winning.

And then you look at your bank account — and your stomach drops.

How is this possible? How can a business be profitable and still feel broke?

I want to answer that question today — clearly, honestly, and in a way that actually helps you do something about it. Because this isn't just a financial puzzle. For many business owners, it's a source of genuine anxiety and confusion that deserves a real answer.

Profit and Cash Are Not the Same Thing

This is the truth that changes everything, and it's the one most business owners were never taught.

Profit is an accounting number. It's the difference between your revenue and your expenses — calculated according to accounting rules that don't always care about when money actually moves.

Cash is reality. It's the actual dollars sitting in your bank account right now — available to pay your team, your vendors, your rent, and yourself.

Here is the critical insight: your accounting records income when it is earned, not when it is received. So the moment you send an invoice, that revenue hits your P&L. Your business looks profitable. But if your client doesn't pay for thirty or sixty days, that cash doesn't exist yet — and meanwhile, your bills are very real and very due.

A U.S. Bank study found that poor cash flow management is the reason 82% of small businesses fail — not lack of profit, not lack of customers, not lack of hard work. Cash flow.

The Five Reasons Profitable Businesses Run Dry

Understanding why this happens is the first step toward fixing it. Here are the five most common culprits.

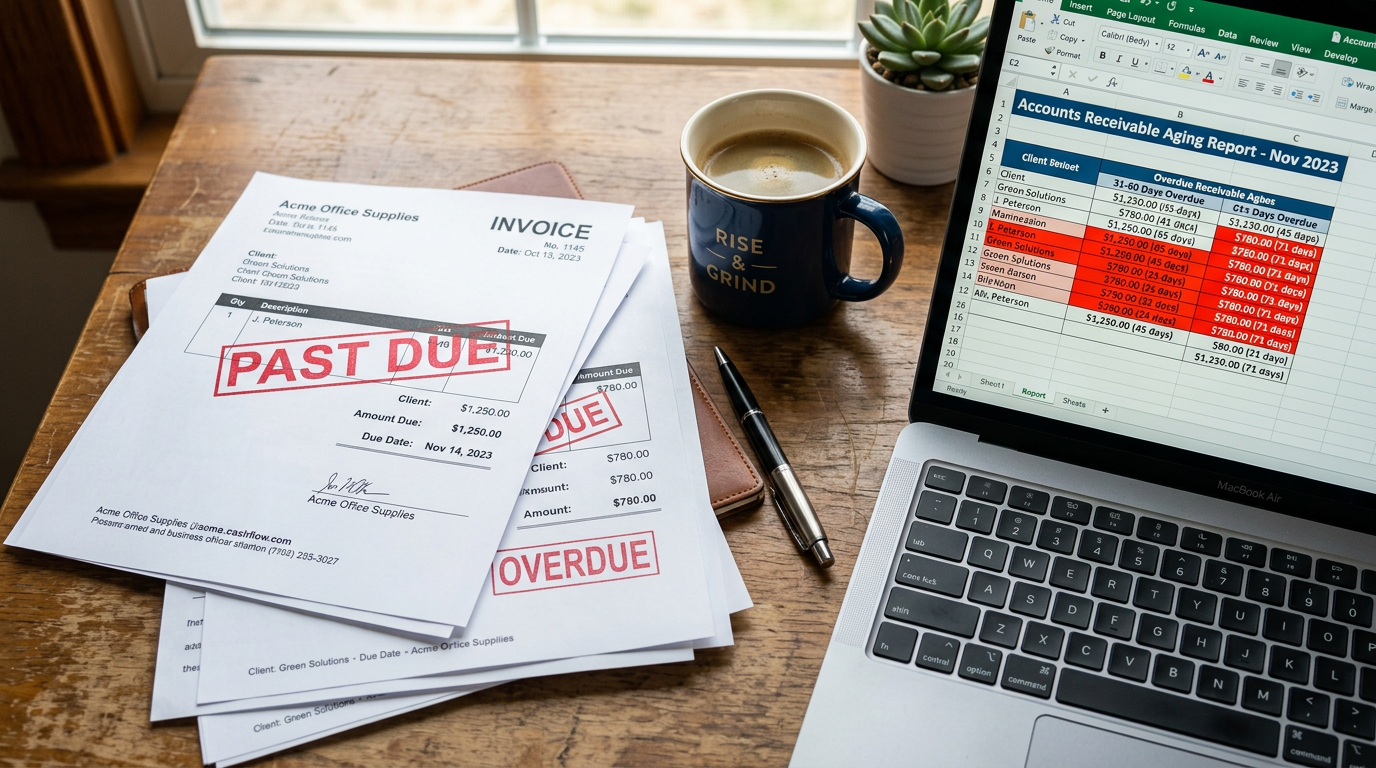

1. Slow-Paying Customers (Accounts Receivable)

This is the most common cause. When you extend payment terms — Net 30, Net 60, even Net 90 — you've made the sale but you haven't received the money. Your P&L celebrates the win. Your bank account waits.

If your receivables are growing faster than your collections, you are essentially lending money to your customers — with no interest, and no certainty of timing — while your own obligations come due on schedule. The faster you grow, the worse this problem can become.

2. Inventory Tying Up Working Capital

If your business carries physical inventory, every dollar spent buying product is a dollar that disappears from your bank account before the sale happens.

You may have $50,000 sitting on shelves that your P&L counts as an asset — but you can't pay payroll with inventory. Overstocking or carrying slow-moving products locks real cash in your warehouse instead of your account, and it can quietly drain a business that looks perfectly profitable on paper.

3. Debt Payments That Don't Show on Your P&L

This one surprises business owners every time they first encounter it. When you repay the principal on a loan, that payment does not appear as an expense on your Profit & Loss statement. It's a balance sheet transaction.

But the cash is absolutely, definitely leaving your account. So your P&L might show healthy profitability while your actual cash is being steadily consumed by loan repayments that are completely invisible on the report most owners actually look at.

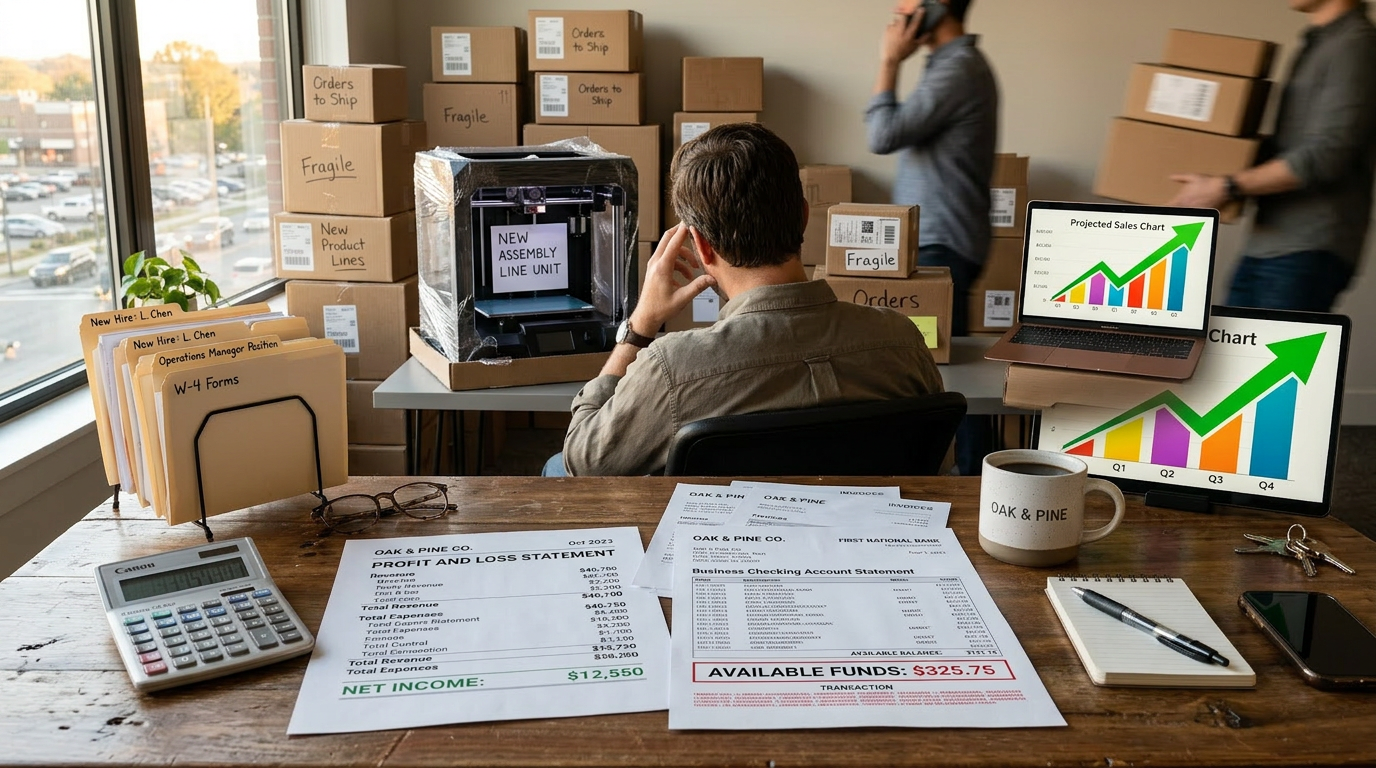

4. Growing Too Fast

Growth is a blessing — until it becomes a cash trap. When your business expands, expenses almost always increase before revenue catches up. You hire people. You buy equipment. You take on overhead. And for a season, you are cash-negative even as your business is objectively succeeding.

One documented case involved a company with $8.7 million in annual profit that went bankrupt — posting negative $1.5 million in cash flow — simply because payment timing created a gap the business couldn't bridge. Growth without cash flow awareness is one of the riskiest seasons a business can navigate.

5. Paying for Expenses Before You Collect Revenue

Many businesses — especially service-based ones — must pay employees, subcontractors, and suppliers before the client pays them. You're funding the work out of your own pocket and waiting to be reimbursed.

When this cycle is short, it's manageable. When clients pay slowly, projects run long, or multiple jobs run simultaneously, the gap between what you've spent and what you've collected can grow into a genuine crisis — even when your books show impressive revenue.

The Antidote: Know Your Cash Flow Cycle

Every business has a cash flow cycle — the time it takes from spending money to receiving money back. Understanding yours is one of the most important things you can do as a business leader.

Ask yourself:

How long does it take from delivering my product or service to receiving payment?

Are my expenses due before or after that cash arrives?

What is the gap — and is it growing or shrinking?

The shorter the gap, the healthier your cash position. The longer the gap, the more working capital you need to bridge it.

Practical Steps to Close the Gap

Once you understand what's causing your cash problem, the solutions become much clearer. Here is where to start:

Invoice immediately. Every day between completing work and sending an invoice is a day of unnecessary delay. Invoice the moment the work is done.

Shorten payment terms. Net 30 is a courtesy, not a requirement. Net 15 or even payment on delivery is reasonable to request, especially from new clients.

Offer early payment incentives. A small discount for paying within 10 days can dramatically accelerate your cash cycle.

Follow up on late invoices consistently. Accounts receivable over 30 days should receive a friendly, professional follow-up. Over 60 days, a more direct one.

Build a cash reserve. Even one to two months of operating expenses set aside as a cash buffer can protect you from the timing mismatches that catch most businesses off guard.

Review your cash flow statement monthly — not just your P&L. The cash flow statement tells you the truth your P&L can obscure.

A Word From a Financial Shepherd

I've walked alongside enough business owners to tell you that the cash flow trap is one of the most disorienting places a leader can find themselves. You're working hard. You're serving people well. The business is growing. And yet you feel financially stressed — because the cash doesn't match the effort.

That feeling is not a sign that you failed. It's a sign that you need better information and a clearer financial picture.

Good stewardship is not just about earning more. It's about understanding the flow — where the money comes from, where it goes, and when. When you understand your cash flow cycle and manage it intentionally, you move from reacting to leading. From anxiety to clarity.

That's what we help business owners do. At Accounting & Computer Concepts, LLC, we don't just keep your books — we help you understand what your numbers are telling you, so you can lead your business with confidence and peace of mind.

I've had enough of those conversations — the ones where a business owner sits across from me, confused and discouraged, wondering why their hard work isn't showing up in the bank account — that I decided to do something about it. I put together the Cash Flow Clarity Kit: a free, practical guide built for business owners who want to understand their cash flow without needing an accounting degree to do it. If the gap between your profits and your cash has ever kept you up at night, this kit was made for you.